The financial services industry has experienced an ideal shift over the last decade.

Once commanded by brick-and-mortar banks, lending is now enabled by digital platforms that permit individuals to borrow and lend without the need of traditional intermediaries.

Peer-to-peer (P2P) lending apps represent one of the most disturbing forces in this transformation.

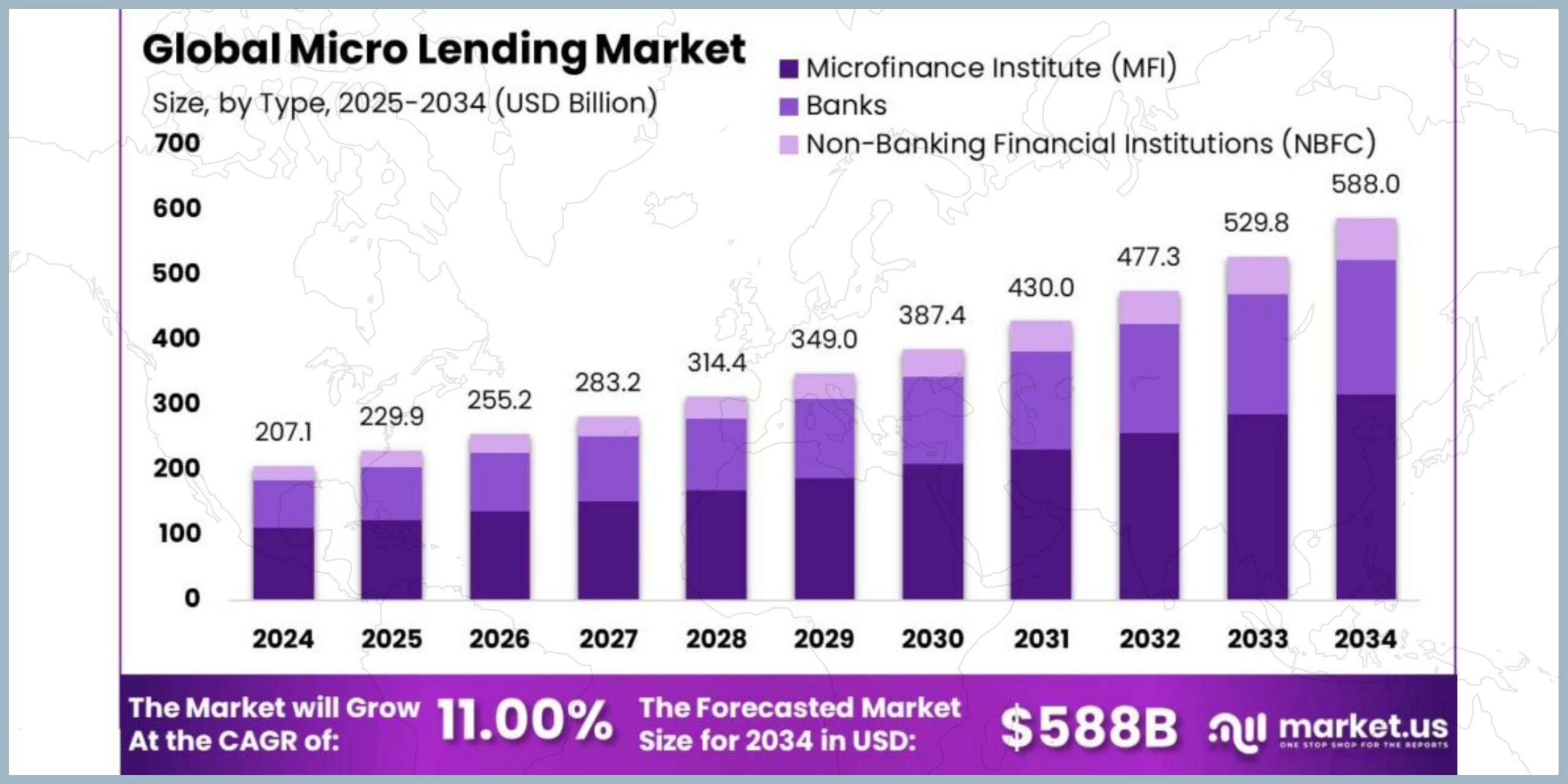

In 2025, the global P2P lending market is expected to surpass $700 billion, fueled by smartphone addiction, real-time payments, AI-driven credit scoring, and blockchain based security.

These apps offer clarity and market-driven pricing which is preferred by consumers.

Launching a P2P lending app offers a future-ready opportunity for startups, entrepreneurs and fintech players.

Borrowers are benefitted from smooth access to credit, inestors enjoys higher returns, and the platform owners can make more profit through variety of channels.

SoftCurators specializes in creating secure and user-friendly fintech app development services.

From initial concept to post-launch maintenance, we help clients design P2P lending apps that meet global compliance standards and excite users with seamless digital experiences.

With our proven approach we will help you turn your vision into a delightful revenue generating application.

What is a P2P Lending App?

A P2P lending app is a digital platform that helps borrowers and lenders to connect directly, eliminating intermediaries like banks.

Borrowers can apply for personal, business or microloans within the app, while lenders can browse the requests and choose where to invest their money to earn higher and attractive interest rates.

By eliminating banking middlemen, P2P lending apps reduce operational cost, which enables favourable loan conditions for both the parties.

Most popular global pioneers, such as LendingClub, Prosper, Zopa, and Funding Circle have already proven the potential and prospectice of this model.

However, the market still has enormous room for confined and specific lending apps, especially in emerging markets such as India, the UAE, and parts of Africa.

The principle of a P2P lending platform lies in clarity, faith, and the technology.

With strong security measures like encoded transactions and KYC-(Know Your Customer) verification, borrowers and lenders can vigorously interact.

This platform ensures compliance with regional financial regulations.

Key components include borrower profiles, risk assessments, interest rate calculations and automated repayment tracking.

These apps eliminate many overhead costs of traditional banking which enables borrowers to enjoy lower rates and lenders gain higher profit than typical savings accounts.

To be more specific:

- Borrowers get easy access to credit often at the better rates.

- Lenders earn higher and attractive interest rates.

- The platform obtain profits through several sources like commissions, service fees, and premium subscriptions.

Why Invest in a P2P Lending App?

📈 Rapid Market Growth

Analysts have projected 28% CAGR from the year 2024-2030 for P2P lending app across the world.

With the excessive increase in smartphone addiction, the demand for mobile-first fintech app has derived.

This wide smartphone adoption has raised internet dispersion in emerging markets and growing consumer confidence in digital business.

Borrowers increasingly prefer the speed and suitability of app based lending over outdated bank loans.

Investors on the other hand are drawn to the higher earnings that P2P platforms offers.

💰 Multiple Revenue Streams

From processing fees, transaction charges to premium subscriptions, A P2P lending platform can offer 5–7 different monetization opportunities.

Equally gripping is the variety of revenue streams accessible to a well designed lending platform.

Unlike a single service financial product, a P2P app can generate income in many ways:

- Origination and processing fees on each loan

- Monthly or annual subscription plans for premium features

- Late payment penalties

In-app purchases such as complete credit reports, even targeted advertising or partnership programs with banks and non-bank financial companies.

With careful planning, a single platform can solve five to seven distinct income channels, reducing dependence on any one source and improving long term profitability.

🌍 Wider Business Reach

Unlike traditional banks restricted by geographic boundaries, a P2P lending app being digital can be operated across borders, attracting borrowers from emerging economies who are in need of funds and investors who are looking for higher returns.

Peer to peer lending apps are now giving a far wider business reach than traditional financial institutions.

The model unites borrowers and investors directly through a digital platform.

A single app can serve users across multiple regions, scaling internationally with the right agreement framework.

This cross-border potential is mainly attractive in developing economies where credit access is limited and in markets where investors seek higher returns.

By bringing together digital availability with the confined monitoring support, a P2P lending app can quickly move outside national boundaries and capture a worldwide customer base.

In short, we can be assured that the accelerating growth of the P2P sector, the availability of multiple profitable paths and the ability to operate on an international scale creates a powerful business case for investing in a peer-to-peer lending app in the coming year.

This borderless reach gives entrepreneurs access to an ever-growing global user base.

SoftCurators can help you to get the most out of on these developments, creating a platform with the adaptability, security and feature set required to stand out in the competitive fintech landscape.

Key Features of a Successful P2P Lending App

Must Have Features

- User Registration & KYC Verification – Secure onboarding with borrower/lender profiles.

- Loan Listings with Details – Transparent loan offers with terms & conditions.

- Loan Processing & Disbursement – Instant fund transfers via Machine-driven approval workflows.

- Investment & Loan Management Dashboard – All-in-one tools to track multiple investments, repayments and profits.

- Interest & Returns Calculator – Quick insights into repayment amounts and ROI.

- Secure Payment Gateway – Seamless repayment and investment transactions.

- Transaction Tracking – Transparency in every fund movement.

- Help & Support (24/7 Chat & Call) – Dedicated fintech support.

Advanced Features

- AI-based Credit Scoring → Automated risk analysis.

- Smart Lending Recommendations → Match borrowers with ideal lenders.

- Real-time Notifications → Loan status updates.

- Biometric Authentication → Fingerprint/Face ID for improved security.

- Blockchain-powered Smart Contracts → Rigid lending agreements.

- Integrated eWallets → Faster transactions without bank delays.

Technology Stack for P2P Lending App Development

At SoftCurators, we employ a modern tech stack that accommodates adaptability, accuracy, and safety for the users:

| Frontend | React Native, Flutter, Swift (iOS), Kotlin (Android) |

| Backend | Node.js, Django, Ruby on Rails, .Net |

| Database | PostgreSQL, MongoDB |

| Payments | Stripe, PayPal, Razorpay APIs |

| Security | Biometric APIs, Blockchain, 256-bit encryption |

| Cloud | AWS, Google Cloud, Azure |

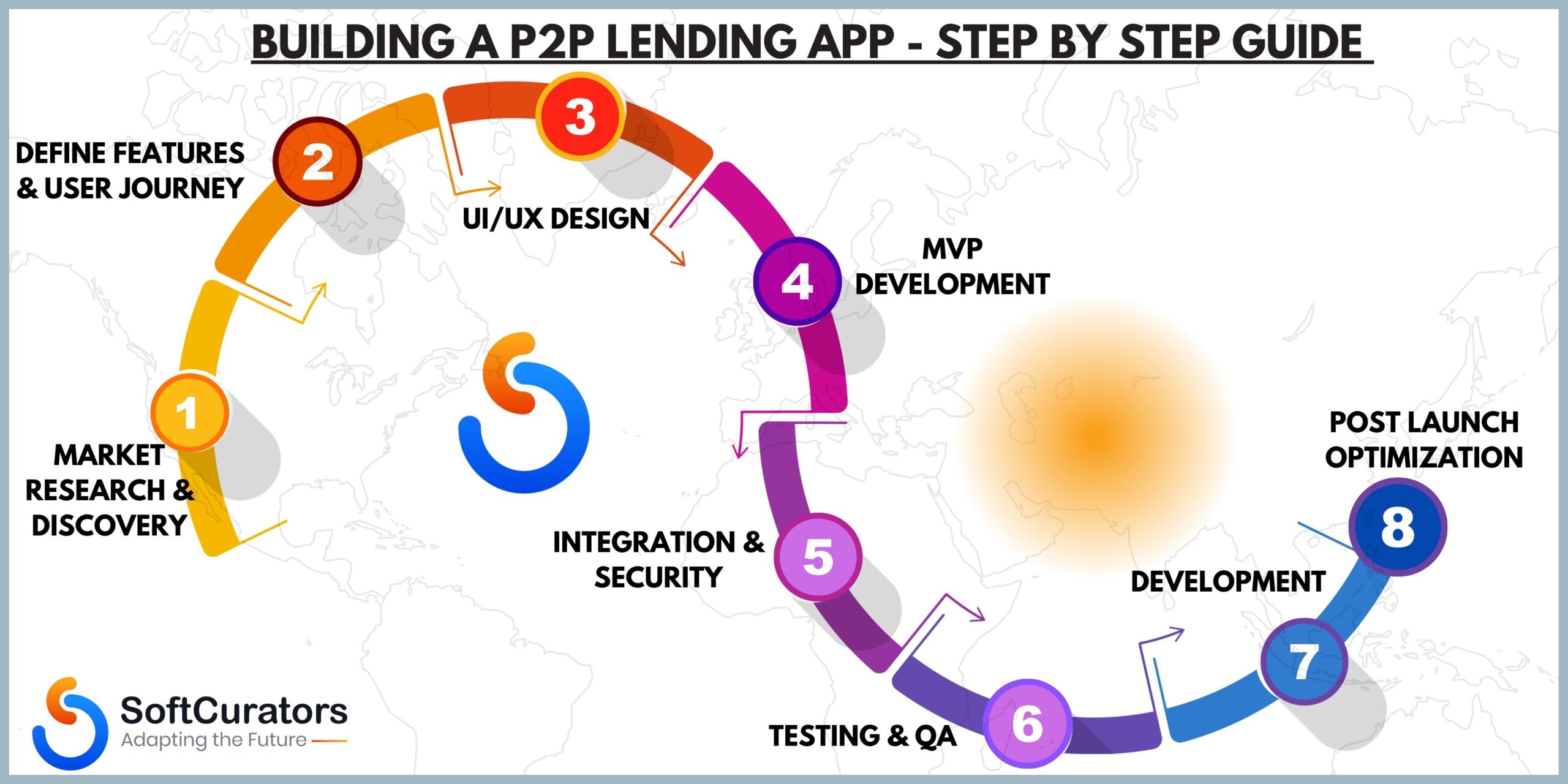

Step-by-Step Process to Develop a P2P Lending App

Step 1: Market Research & Compliance Analysis

Developing a lending app begins with the accurate market research and compliance analysis as you need a deep understanding of the lending background in your targeted regions.

This includes identifying potential borrowers and investors and studying competing platforms to learn which features, fees, and credit valuation methods are most effective.

At the same time, legal and regulatory requirements should also be evaluated.

Step 2: UI/UX Wireframing & Design

The next stage includes user experience drafting and visual design where designers create wireframes and prototypes.

From identity verification to funding, repayments and portfolio tracking, these prototypes are tested with real users to improve navigation and streamline KYC steps.

This refined design system guides developers and maintains brand reliability across devices.

Step 3: MVP Development

With a confirmed design in hand, the team moves on to minimum viable product development.

The MVP focuses on the essential functions that prove the concept in a live environment.

Core capabilities such as secure user registration, loan listing and matching, payment integration, and basic credit-scoring logic are implemented first.

A robust backend is set up with APIs and database schemas while security basics like encrypted data transfer, role-based access, and audit logging are established to protect financial information from the start.

Step 4: Integration of Advanced Features (AI, Blockchain, ML)

After the MVP establishes product market fit, advanced technologies can be layered into a distinct platform.

Artificial intelligence and machine learning models enhance credit risk analysis and fraud detection.

Blockchain smart contracts can be added to provide automated settlements.

At this stage it is common to introduce human in the loop oversight for AI models.

Step 5: Testing & Quality Assurance

Comprehensive testing and quality assurance follow in the next step. The app is subjected to challenging functional and security testing.

Testing of unit and integration checks to penetration tests are done. Payment flows, loan distributions, and data privacy controls are validated.

Step 6: App Store Deployment (iOS & Android)

When the app finally permits the quality checks, it is settled for release on the iOS App Store and the Google Play.

This involves building signed binaries, creating store listings with clear privacy policies, and satisfying financial category review requirements.

Step 7: Post-Launch Support & Maintenance

At the last, post launch support and maintenance become an ongoing restraint. Real time monitoring tools track uptime, transaction success rates and key business metrics such as investor retention.

While Customer support teams handle questions and repayment issues, the developers on the other hand, checks for regular updates, security patches, and feature developments.

With the combination of active observing, reactive customer care and controlled development practices this platform remains secure and trusted as it grows.

Step 8: Cost to Develop a P2P Lending App

Development cost depends on the features, region and the tech stack which are used to build a lending app.

Factors Affecting Cost:

| Features & Integration |

| Region of development (India: $15-$30/hr- US/Europe: $100-$200/hr) |

| UI/UX Complexity |

| Compliance requirements (AML, KYC, GDPR) |

Average Cost Range

| Basic P2P Lending App | $15,000 – $25,000 |

| Medium Complexity App | $25,000 – $50,000 |

| Advanced App (AI, Blockchain) | $50,000 – $100,000+ |

How Do P2P Lending Apps Make Money?

Revenue models for P2P lending platforms comprise:

- Origination Fees – Processing fees on loans.

- Service Charges & Penalties – Late payment fees.

- Subscription Plans – Premium features for lenders/borrowers.

- In-app Purchases – Credit reports, financial insights.

- Advertisements – Third-party financial services ads.

- Partnerships with Banks & NBFC Hybrid models.

Compliance, Security & Regulatory Requirements

| KYC/AML Integration (Know your customer & Anti-Money Laundering) |

| GDPR & CCPA Data Protection |

| PCI DSS Payment Security |

| Blockchains and Smart Contracts |

Compliance is non-negotiable. At SoftCurators, we integrate legal, security, and financial compliance from day one.

Latest Trends in P2P Lending App Development

- AI-driven Credit Risk Analysis

- Blockchain powered Smart Lending Contracts

- Buy Now Pay Later-(BNPL) Integration

- Voice-enabled Loan Applications

- Decentralized Finance (DeFi) Lending Apps

Why Choose SoftCurators for P2P Lending App Development?

At SoftCurators, we don’t just build apps — we build scalable fintech ecosystems.

✔️ Expertise in P2P Lending, BNPL, and Fintech App Development

✔️ Proven experience in secure payment gateway integration

✔️ Custom development tailored to your business model

✔️ Agile process with MVP-first approach

✔️ Post-launch support for scaling & updates

👉 Explore our Fintech App Development Services to get started.

Conclusion

The future of lending is digital, propagated, and user-first. Building a P2P lending app is not just about technology, it’s about reliability, security, and compliance.

With the right strategy, features and development partner like SoftCurators, your lending platform can become the next LendingClub or Prosper and maybe even bigger.

FAQs

- What are the must have features of a P2P lending app?

User onboarding, loan listings, secure payment gateway, AI-based credit scoring, investment dashboards and biometric authentication.

- How does the P2P lending business model work?

Borrowers request loans, lenders invest, and the platform acts as a facilitator earning through fees and subscriptions.

- What is the average cost of developing a P2P lending app?

Anywhere from $25,000 to $300,000+ depending on complexity and region of development.

- How do P2P lending apps ensure security?

Through KYC/AML verification, encryption, biometric authentication and blockchain powered smart contracts.

- Can a P2P lending app be integrated with BNPL services?

Yes, modern lending platforms often participate in Buy Now Pay Later-(BNPL) to attract more users.

- Which technologies are the best fit and reliable for building a P2P lending app?

Technologies like React Native or Flutter should be preferred for frontend, Node.js or Django will be best for backend, and AWS or Google Cloud will be reliable for scaling.

- Why choose SoftCurators for fintech app development?

We combine technical expertise, compliance-first approach, and fintech innovation to deliver secure and scalable lending apps.